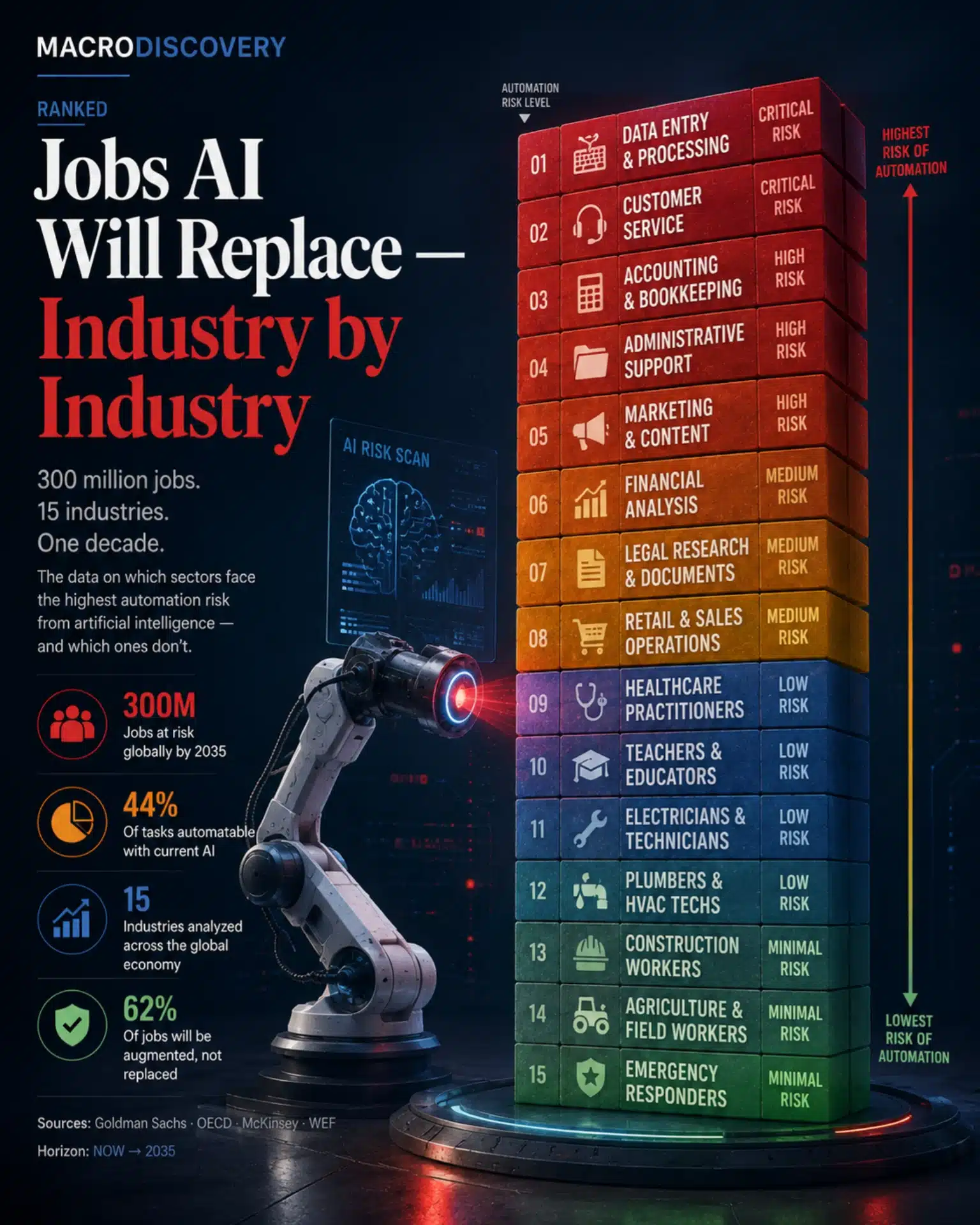

Jobs AI Will Replace —

Industry by Industry

300 million jobs. 15 industries. One decade. The data on which sectors face the highest automation risk from artificial intelligence — and which ones don’t.

Share of jobs at high automation risk within each sector. Based on task-level analysis across 900+ occupations.

Disruption does not arrive all at once. Each sector has a window. Source: McKinsey Global Institute, OECD 2024.

2024

–2028

–2033

–2040

The question is not whether AI will displace workers. The data on that is settled. The more useful question is which workers, in which industries, on what timeline — and what the evidence actually shows about the shape of the disruption.

Three major research institutions — Goldman Sachs, McKinsey Global Institute, and the OECD — have now published task-level analyses of AI automation exposure across hundreds of occupations. Their methodologies differ, but their conclusions converge on a consistent picture: the first wave is already underway, it is hitting cognitive routine work hardest, and the peak displacement decade is 2025–2035.

“The jobs most at risk are not the ones that require the least education. They are the ones that require the most repetitive cognition — regardless of salary or credential.”

The Counterintuitive Finding

What the Data Does Not Say

The 300 million figure — jobs at high automation risk globally — is frequently misread as 300 million jobs that will disappear. This is not what the research shows. Task-level analysis measures the proportion of tasks within a job that are automatable, not whether the entire job disappears. A financial analyst whose 60% of tasks are automatable may see their role transform — fewer hours spent on routine analysis, more on judgment, client relationships, and interpretation — rather than eliminated entirely.

The WEF’s Future of Jobs Report 2025 estimates that while 85 million jobs may be displaced by automation by 2030, approximately 97 million new roles may emerge — net job creation, not net destruction, driven by the green economy, AI infrastructure, and care sector expansion driven by aging demographics.

The more precise concern is transitional dislocation: the gap between the speed of displacement and the speed of workforce adaptation. Historical technology transitions — the industrial revolution, electrification, computerization — all ultimately created more jobs than they destroyed. They also created significant human hardship in the transition period, concentrated in specific geographies, age groups, and skill sets.

The industries with the highest automation exposure share a common characteristic: they are built on cognitive routines applied to structured data. Administrative work, financial analysis, legal research, and customer service are all, at their core, pattern-matching tasks. Current AI systems are remarkably good at pattern matching. The match between AI capability and job task is unusually tight in these sectors.

The industries with the lowest exposure share a different characteristic: their core value is created in unstructured human contexts — complex physical environments, emotional relationships, trust-dependent interactions, and creative judgment that requires genuine understanding rather than pattern reproduction.

The question for the next decade is not whether AI will be transformative. It will be. The question is whether the educational and social systems that prepare workers for the labor market can adapt fast enough to match the pace of the technology. Based on historical precedent, the answer is: probably not fast enough to prevent significant disruption — but ultimately yes.