The Map of

Nuclear Energy Today

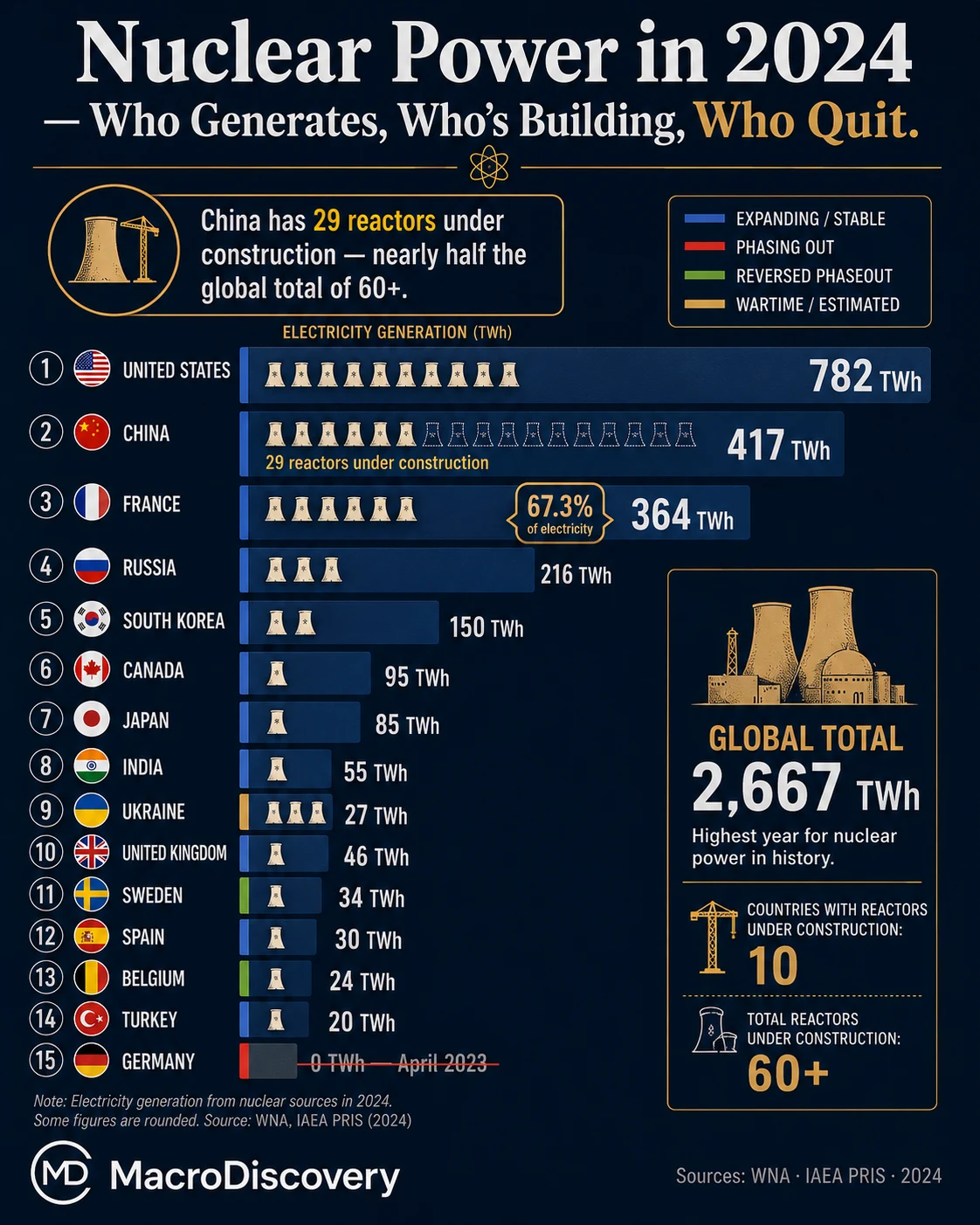

The US generates more nuclear electricity than the next three countries combined. France runs two-thirds of its grid on nuclear. China is building 29 new reactors simultaneously. Germany shut its last plant in 2023. And 2024 was the biggest year for nuclear power in history.

Nuclear power divides the world into three camps: countries that are expanding it aggressively, countries that are winding it down, and countries that have quietly reversed course after decades of opposition. The 2024 data — the best year for nuclear generation in history — shows all three groups clearly. What they have in common is that every one of them is reconsidering where nuclear fits. Many policymakers argue that wind and solar alone may not be sufficient to provide reliable electricity at scale without complementary technologies — whether that means storage, flexible generation, expanded transmission, or nuclear.

- 2024 was the highest year for nuclear generation ever recorded — 2,667 TWh globally, surpassing the previous record set in 2006 by 7 TWh. The record reflects fleet life extensions, improved capacity factors, and new builds in China and the US.

- The US generates 782 TWh from 94 reactors — nearly 30% of all nuclear electricity on earth — and runs its fleet at a 92% capacity factor, the highest of any major electricity source globally.

- France gets 67.3% of its electricity from nuclear — the highest share of any large economy. After corrosion-related repairs collapsed output to ~282 TWh in 2022, the fleet rebounded to 364 TWh in 2024. France is now planning at least six next-generation EPR2 reactors.

- China has 29 reactors under construction — nearly half the global total — adding to 57 already operating. Its nuclear output grew 4% in 2024 and will accelerate sharply as new units come online through the decade.

- Germany and Taiwan both exited nuclear — Germany in April 2023, Taiwan in May 2025. Both decisions remain politically contested. Germany now burns more coal than it did before the phaseout began.

| # | Country | 2024 TWh | Nuclear Share | Reactors | Status / Note | Share |

|---|---|---|---|---|---|---|

| 1 | 🇺🇸United States |

782.0 | 18.2% | 94 · 97 GW | Vogtle 3&4 online | |

| 2 | 🇨🇳China |

417.5 | 4.9% | 57 · 59 GW +29 UC | Fastest expansion | |

| 3 | 🇫🇷France |

364.0 | 67.3% | 57 · 63 GW | EPR2 expansion planned | |

| 4 | 🇷🇺Russia |

202.1 | 21.8% | 34 · 28 GW +5 UC | Rosatom exporting globally | |

| 5 | 🇰🇷South Korea |

179.4 | 30.1% | 26 · 26 GW +2 UC | APR-1400 export model | |

| 6 | 🇯🇵Japan |

84.9 | 8.7% | 14 · 13 GW | Slow restart post-Fukushima | |

| 7 | 🇨🇦Canada |

81.2 | 14.8% | 17 · 13 GW | CANDU fleet · SMR planned | |

| 8 | 🇪🇸Spain |

52.1 | 20.7% | 7 · 7.1 GW | Phase-out by 2035 | |

| 9 | 🇺🇦Ukraine |

~50 est. | ~55% | 15 · 13 GW | Wartime · data estimated | |

| 10 | 🇮🇳India |

49.9 | 3.1% | 23 · 7.7 GW +6 UC | +13.4% YoY · fastest growth | |

| 11 | 🇸🇪Sweden |

48.7 | 30.8% | 6 · 7.0 GW | Phase-out reversed | |

| 12 | 🇬🇧United Kingdom |

37.3 | 13.9% | 9 · 5.9 GW +2 UC | Hinkley C delayed to 2029–31 | |

| 13 | 🇫🇮Finland |

31.1 | ~40% | 5 · 4.4 GW | Olkiluoto-3 stabilised 2024 | |

| 14 | 🇧🇪Belgium |

29.7 | 50.3% | 2 · 2.1 GW | Phase-out reversed · 10-yr ext. | |

| 15 | 🇨🇿Czech Republic |

28.0 | 36.2% | 6 · 4.0 GW | New build approved |

Source: World Nuclear Association — “Nuclear Generation by Country” (September 2025 update) and “Global Nuclear Industry Performance” Annual Report 2024, citing IAEA Power Reactor Information System (PRIS), US Energy Information Administration, and company data. All figures are 2024 full-year generation. Reactor counts and capacity from IAEA PRIS (late 2025). Click column headers to sort.

Ukraine’s 2024 generation figure is explicitly flagged as estimated by the WNA due to the ongoing conflict. Share figures show what fraction of each country’s total electricity came from nuclear in 2024. UC = under construction. Note: The UAE generated approximately 36.5 TWh in 2024 from its four Barakah reactors — which would place it between the UK (37.3 TWh) and Finland (31.1 TWh) in this table. The UAE figure is from secondary sources citing WNA data and is not confirmed from the official WNA ranked table.

The US Fleet: Old, Efficient, and Still Irreplaceable

America’s 94 nuclear reactors were mostly built between 1967 and 1990. They are, on average, over 40 years old. And yet in 2024 they generated 782 TWh at a capacity factor of 92% — the highest reliability rate of any major electricity source anywhere in the world. Typical wind and solar capacity factors are substantially lower than the US nuclear fleet’s 92%. The US nuclear fleet is the single largest source of low-carbon electricity in the Western hemisphere and it operates with a consistency that no other technology currently matches at scale.

In 2023 and 2024, the US broke a 40-year drought in nuclear construction. Vogtle Unit 3 connected to the grid in July 2023, Unit 4 in April 2024 — the first large commercial reactors completed in America in decades. They were late and expensive. But they exist. More importantly, they demonstrated that a Western economy can still build large nuclear, and they unlocked federal support for a new generation of smaller modular reactor designs being developed by companies including TerraPower, X-energy, and NuScale. The US is simultaneously the world’s largest nuclear generator and, very slowly, restarting its construction pipeline.

France: The World’s Most Nuclear-Dependent Large Economy — and Its Turbulent Recent History

In 2022, France’s nuclear output collapsed to around 282 TWh — its lowest level in decades — after a combination of stress-corrosion cracking discovered in dozens of reactor cooling circuits and scheduled maintenance outages hit simultaneously. The country that had built its entire energy identity around nuclear suddenly found itself importing electricity from Germany, which was burning coal to keep the lights on, in order to supply French homes.

By 2024 the fleet had largely recovered: 364 TWh generated, with 67.3% of France’s electricity coming from nuclear — still the highest share of any large economy in the world. France has now committed to building at least six new EPR2 reactors (an improved version of the European Pressurised Reactor design) and is studying the case for up to fourteen. The French model — standardised reactor designs, centralised regulation, long-term commitment — built 52 reactors in 15 years during the 1970s and 1980s and remains one of the clearest historical examples of rapid, large-scale nuclear deployment.

China Is Building Half the World’s New Nuclear

China currently has 29 reactors under construction — nearly half of the global total of over 60. It already operates 57, generating 417.5 TWh in 2024 with a nuclear share of just 4.9% of its vast total electricity consumption. That low share is not a sign of weakness — it reflects how much electricity China generates in total. The country’s nuclear ambition is to raise that share significantly, and it is doing so by building at a pace no other country is close to matching.

China’s strategy is standardisation. Rather than designing bespoke reactors for each site — which drove cost and schedule overruns in Europe and the US — China selected a small number of proven designs (principally the domestically developed Hualong One, or HPR-1000) and is building them in parallel across multiple sites simultaneously. Construction times have fallen steadily. The approach is the closest any country has come to replicating France’s 1970s build programme. Of the 68 reactors commissioned worldwide over the past decade, 56 were built in Asian countries — a figure confirmed directly in the WNA World Nuclear Performance Report 2025. The trajectory is clear.

Germany, Taiwan — and the Countries Changing Their Minds

Germany shut its last three reactors in April 2023, completing a phaseout that began after Fukushima in 2011. The decision was fiercely contested at home and abroad. Germany’s coal consumption has continued falling since the phaseout — down sharply in both 2023 and 2024 according to official data from AGEB, Germany’s Working Group on Energy Balances, driven by weaker industrial output, rising renewables, and higher carbon prices. The debate is not primarily about coal returning; it is about whether the grid has sufficient reliable backup on days when wind and solar underperform, and about whether the phaseout raised electricity prices and weakened energy security at a geopolitically sensitive moment. Germany now imports more electricity than it exports. The political debate about whether the decision was correct has not ended.

Taiwan closed its last operating reactor in May 2025, completing a phaseout that began in the mid-2010s. Both exits — Germany and Taiwan — have since been challenged by the same structural reality: grids that run on variable renewables alone need something to cover the gaps when the wind doesn’t blow and the sun doesn’t shine. That something is currently fossil fuel in both countries.

The counter-movement is visible. Belgium reversed its nuclear phaseout and extended the operational life of two reactors by ten years. Sweden reversed its phaseout and is planning new builds. Japan, which had nearly shut down its entire fleet after Fukushima, has restarted 14 reactors with more to follow. The Czech Republic has approved a new nuclear build and selected Korea’s KEPCO as preferred supplier. The political calculus around nuclear power has shifted more in three years than in the previous twenty.

The UAE and South Korea: A New Export Model

South Korea’s APR-1400 reactor design has become the world’s most successful nuclear export in a generation. The four-unit Barakah plant in the UAE — built by a Korean-led consortium under KEPCO — reached full operational capacity in 2024, generating approximately 36.5 TWh. That output would place it between the UK and Finland in the global ranking. Barakah was completed broadly on schedule — an achievement rare enough in the modern nuclear industry that it is studied as a case study in how standardised, pre-approved designs and experienced construction teams can deliver what many bespoke Western projects have struggled to match.

South Korea is now the preferred supplier for the Czech Republic’s planned expansion, is in discussions with Poland, and is being evaluated by several other Central European governments. Russia’s Rosatom has long dominated nuclear exports — building or financing plants in Turkey, Egypt, Bangladesh, and India — but South Korea’s commercial model, without the geopolitical complications of a Russian contract, is increasingly competitive. The geography of who builds the world’s next generation of nuclear plants will shape energy and alliance relationships for decades.

- World Nuclear Association — “Nuclear Generation by Country” (updated September 2025 · citing IAEA PRIS + EIA + company data)

- World Nuclear Association — “Global Nuclear Industry Performance” Annual Report 2024 (2,667 TWh global record · 83% capacity factor · 7 new grid connections)

- World Nuclear Association — “Nuclear Power in the World Today” (France 67.3% · Ukraine data estimated · Taiwan last reactor May 2025)

- World Nuclear Association — “World Nuclear Power Reactors & Uranium Requirements” (reactor counts · capacity · under construction · Ukraine footnote)

- IAEA Power Reactor Information System (PRIS) — primary reactor capacity and status data (updated June 2026)

- US Energy Information Administration — “Five countries account for 71% of the world’s nuclear generation capacity” (June 2025 · US 94 reactors · 97 GW · 782 TWh · 92% capacity factor)

- IAEA — “Six Global Trends in Nuclear Power You Should Know” (January 2026 · France 67.3% · Slovakia 60.6% · Hungary 47.1% · Finland 39.1%)

- Economy Insights — “Nuclear Energy by Country” (October 2025 · secondary presentation of WNA 2024 data · UAE ~36.5 TWh · Russia ~202 TWh · cited for context)