The Demographic Cliff Nobody’s Priced In

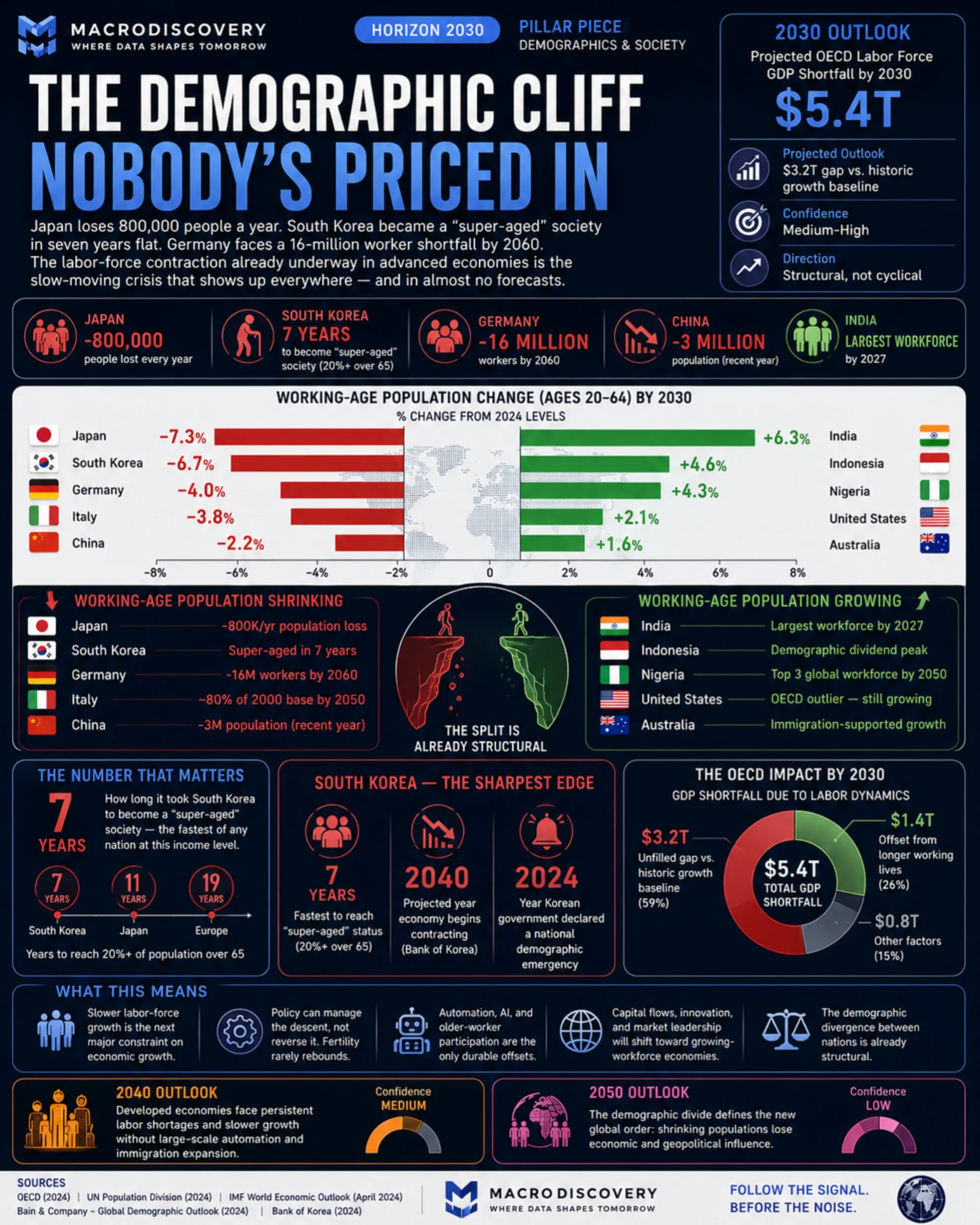

Japan loses 800,000 people a year. South Korea became a “super-aged” society in seven years flat. Germany faces a 16-million worker shortfall by 2060. The labor-force contraction already underway in advanced economies is the slow-moving crisis that shows up everywhere — and in almost no forecasts.

Demographics move too slowly for a news cycle and too fast to fix once noticed. By the time a working-age decline shows up in GDP data and bond markets, it’s been locked in for 20 years by fertility decisions that no policy can reverse in time. That’s why several of the world’s largest economies are already operating under a structural labor-force constraint that almost no near-term economic model fully prices in.

Known — Japan’s population has been shrinking for years — losing more than 800,000 people annually at recent rates. South Korea became a “super-aged” society (20%+ of the population over 65) by the end of 2024, in roughly seven years, compared to Japan’s eleven and Europe’s nineteen. Germany faces a projected decline of 16 million workers between now and 2060.

Projected — Bain & Company’s labor analysis projects that slower OECD labor-force growth could produce a $5.4 trillion GDP shortfall by 2030 versus the historic baseline — with only $1.4 trillion potentially offset by older workers staying in the workforce longer.

Speculative — how much automation and AI-driven productivity growth offsets the labor supply contraction, and how quickly, is the critical unknown this piece cannot resolve. Countries that successfully substitute capital for missing labor may escape the GDP shortfall; those that don’t, won’t.

This Is Structural, Not Cyclical

The critical distinction in demographic analysis is between a cyclical slowdown — which policy can address — and a structural constraint baked in by decades of sub-replacement fertility. No large nation has returned to replacement-level fertility after a prolonged sub-replacement period through policy alone. The mechanisms governments reach for — cash incentives, parental leave, childcare subsidies — show modest, temporary effects at best. What actually shifts fertility rates at scale, historically, is economic development in the other direction: as countries get richer and more educated, fertility falls further.

The implication is that the countries already below the cliff edge aren’t going to climb back up it. The realistic policy options are limited to managing the descent — extending working ages, scaling immigration, improving older-worker participation rates, and accelerating automation — rather than reversing it.

South Korea Is the Sharpest Edge

No developed economy illustrates the demographic cliff more starkly than South Korea. It holds the world’s lowest fertility rate, and its aging acceleration is the fastest ever recorded for a country at its income level. The Bank of Korea’s own modelling warns that if the decline in South Korea’s working population continues at current rates, the economy could begin contracting by 2040 — shifting from its current 2% growth to outright shrinkage within 14 years. The Korean government declared a national demographic emergency in 2024, a signal of institutional seriousness that most governments facing similar trajectories have not yet matched.

The Countries That Escape This — and How

Not every major economy faces a labor-force contraction. India is on track to surpass China as the world’s largest workforce by 2027, and its demographic dividend — a young, large, and growing working-age population — gives it a structural growth tailwind that no amount of investment alone replicates. Indonesia is near its own demographic dividend peak. Nigeria, despite its governance challenges, will have one of the world’s three largest workforces by 2050.

Among OECD economies, the United States is an outlier — still growing its working-age population, primarily through immigration, with fertility that, while below replacement, is higher than most of its peers. Australia follows a similar pattern. These two are the exception within the advanced economy club, not the rule. The structural divergence between shrinking advanced economies and growing emerging ones is itself a macro trend that runs through everything from capital flows to geopolitical leverage over the next two decades.

What This Actually Tells You

Demographics aren’t a future risk — they’re a present constraint operating in slow motion. The labor-force contractions already underway in Japan, South Korea, Germany, Italy, and China will compound through the 2030s regardless of what policies are enacted now. The $5.4 trillion GDP shortfall figure isn’t a prediction of catastrophe — it’s a projection of a structural gap between what these economies would produce with historic labor-force growth and what they’ll produce without it. Filling that gap with automation, immigration, and productivity gains is the actual economic challenge for most advanced economies this decade. Whether they do it successfully is the 2040 and 2050 story, not the 2030 one.