Lithium, Cobalt

and Rare Earths —

The New Oil Map

The energy transition was supposed to reduce dependence on geopolitically volatile resources. Instead it created new dependencies — more concentrated, more fragile, and controlled by fewer countries than oil ever was. The map of the 21st century’s power is drawn in lithium, cobalt, and rare earths.

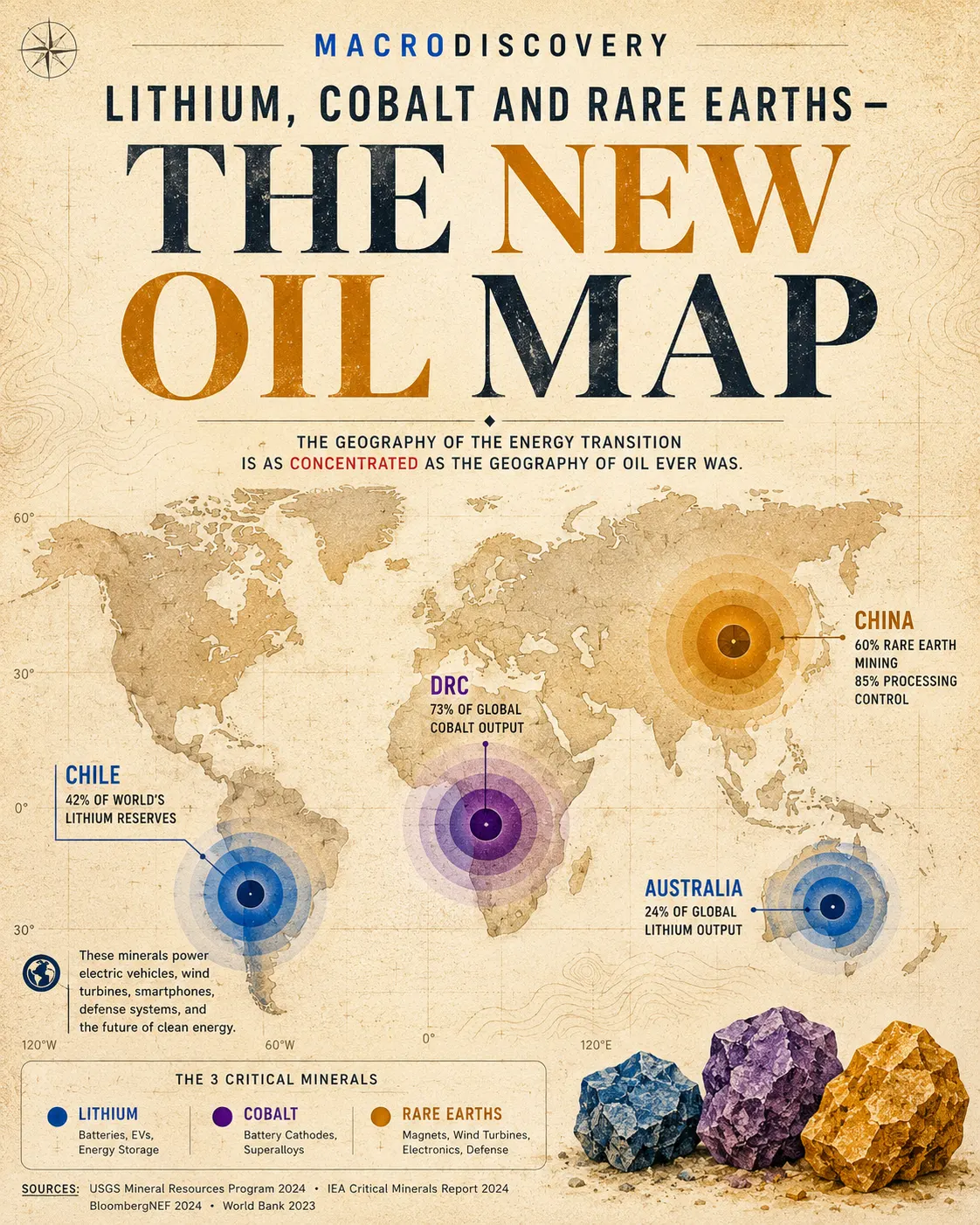

Key deposit locations for lithium (blue), cobalt (purple), and rare earth elements (amber). Circle size indicates relative reserve magnitude. Source: USGS Mineral Resources Program 2024.

Share of global production or reserves by country. The fewer countries on the bar, the more geopolitically exposed the supply chain. Source: USGS 2024, IEA 2024.

Indexed to 2020 baseline (=1.0). IEA Sustainable Development Scenario — the path required to meet net-zero targets. Source: IEA Critical Minerals Report 2024.

Assessed across: geographic concentration, political stability of top producers, processing chokepoints, and substitutability. Source: IEA, World Bank, USGS 2024.

The energy transition was designed to break the world’s dependence on geopolitically volatile fossil fuel producers. The irony visible in the data above is that it has created dependencies that are, in several dimensions, more concentrated than oil ever was. At the peak of OPEC’s power in the 1970s, the cartel controlled roughly 55% of global oil exports. A single country — China — controls 85% of rare earth refining. One province in one country — Katanga in the DRC — produces nearly three-quarters of global cobalt. This is not a diversified supply chain. It is a series of single points of failure embedded into every electric vehicle, wind turbine, and grid battery being manufactured today.

What makes this structurally different from the oil era is the processing chokepoint problem. Oil is a commodity that moves from wellhead to refinery to consumer across dozens of countries. Rare earths and battery minerals require highly specialized processing infrastructure — separation, refining, and chemical conversion — that took China 30 years and enormous state subsidy to build. Even when ore is found in politically friendly nations like Australia or Canada, it often travels to China for processing before returning as usable material. Mining sovereignty and processing sovereignty are different things, and the world currently has only one of them for the most critical minerals.

“China’s export restriction on graphite in 2023 was the first direct test of battery mineral weaponization. It will not be the last.”

The demand forecasts make the urgency structural rather than theoretical. Meeting net-zero scenarios requires building new mines at a pace the industry has never achieved. A typical lithium mine takes 16 years from discovery to production, according to the IEA. The window between when demand curves sharply upward and when new supply can realistically come online creates a decade of price volatility and supply insecurity that will shape which countries can manufacture electrified products at competitive cost — and which cannot.

Three structural shifts will define the critical minerals landscape by 2035. First, chemistry substitution: battery manufacturers are actively engineering cobalt out of their supply chains through LFP chemistry and sodium-ion batteries. BYD and CATL are leading this shift — not because LFP is better in every dimension, but because cobalt’s geographic concentration makes it too dangerous to remain central to mass production. The cobalt map will matter less by 2030 than it does today.

Second, processing sovereignty will become the defining geopolitical investment theme of the decade. The US Inflation Reduction Act, the EU Critical Raw Materials Act, and Australia’s Critical Minerals Strategy are all attempting to build Western processing capacity outside China’s sphere — but they are starting from near-zero and facing a 15–20 year infrastructure gap. Third, deep-sea mining — polymetallic nodules in the Pacific contain vast deposits of cobalt, manganese, and nickel — will move from experimental to commercial, with the first licensed operations expected before 2030. The environmental and jurisdictional frameworks for deep-sea extraction remain deeply contested, but the mineral math makes commercial development close to inevitable.