The Map of Frontier Technology Leadership

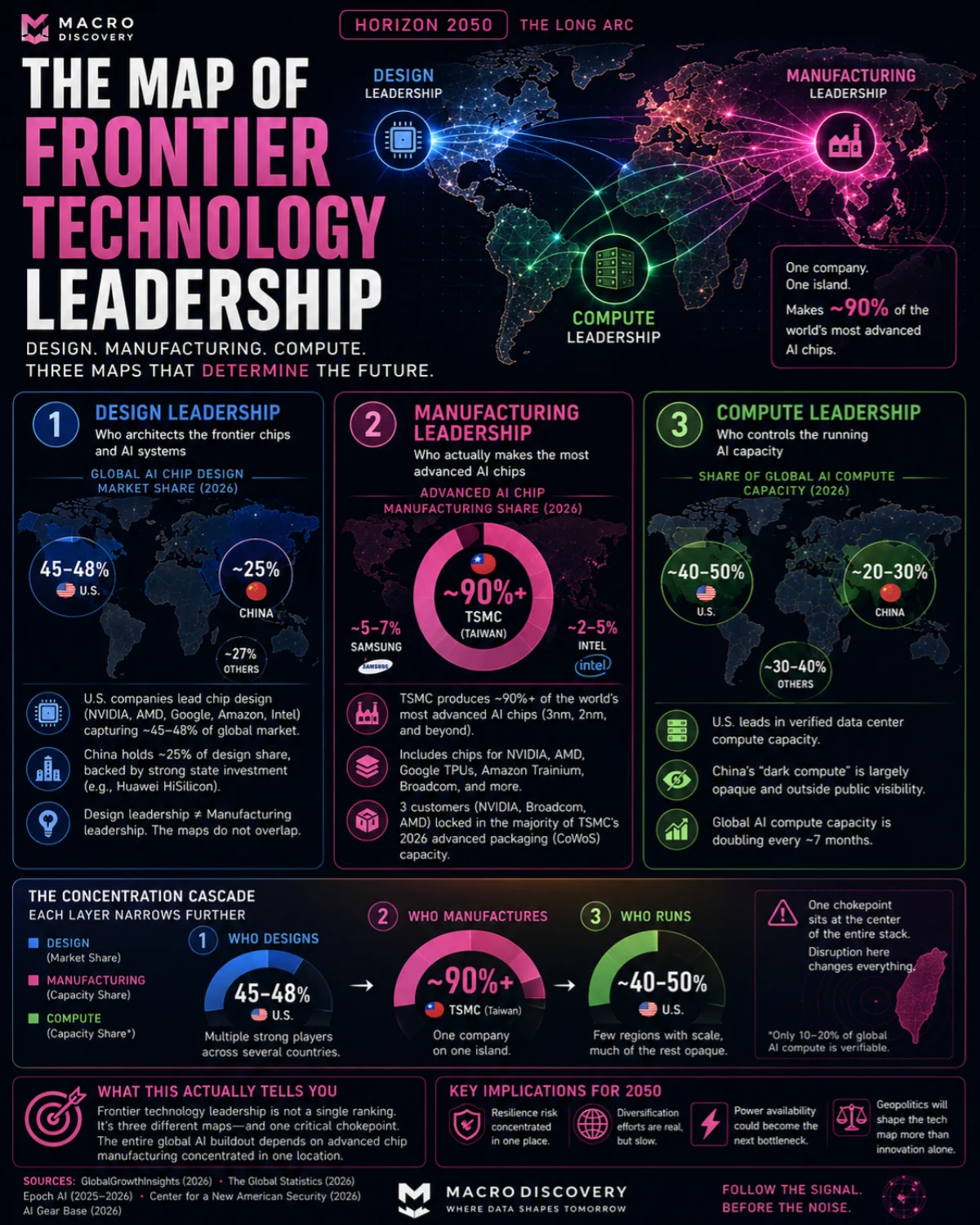

One company, on one island, makes 90% of the world’s most advanced AI chips. That single fact does more to shape who leads frontier technology through 2050 than any country’s AI policy.

Most “who leads frontier technology” stories rank countries by AI investment, patent filings, or model releases. That ranking is real but shallow — it measures who’s spending and publishing, not who actually controls the physical chokepoints that make any of it possible. The deeper map looks completely different, and it has exactly one critical node.

Known — a single company, Taiwan Semiconductor Manufacturing Company, produces the overwhelming majority of the world’s most advanced AI chips — effectively every chip NVIDIA sells, most of AMD’s, most of Google’s TPUs, and Amazon’s Trainium line, all manufactured on one island.

Projected — the United States holds 45-48% of global AI chip design market share and roughly 48% of regional AI chip market share by revenue, with China a distant second at around 25% — but design leadership and manufacturing leadership are not the same map, and the country that designs the most chips isn’t the country that makes them.

Speculative — whether this concentration becomes a permanent structural feature of frontier technology or gets meaningfully diversified by 2050 — through U.S. and EU fabrication investment, or geopolitical disruption forcing the issue — is the open question this entire piece is actually about.

Three Maps, Not One

Design leadership belongs mostly to the United States. American companies — NVIDIA, AMD, Google, Amazon, Intel — architect the chips that define each generation of AI capability, and U.S.-based firms capture roughly 45-48% of global AI chip design market share. China holds a strong second position at around 25%, backed by sustained state investment and companies like Huawei’s HiSilicon, particularly important given that export restrictions have cut off direct access to the most advanced U.S.-designed chips.

Manufacturing leadership belongs almost entirely to one place: Taiwan. TSMC doesn’t just lead chip manufacturing — by several industry estimates, it produces 90% or more of the world’s most advanced AI chips, full stop, regardless of which country designed them. Samsung and Intel both compete for the same tier of advanced manufacturing, but neither currently matches TSMC’s combination of yield, scale, and packaging capacity (the CoWoS technology that allows the high-bandwidth memory modern AI chips require). Three customers alone — NVIDIA, Broadcom, and AMD — have locked in the overwhelming majority of TSMC’s 2026 advanced packaging capacity.

Compute leadership — who actually controls the running AI capacity, not just who makes the chips — sits closer to the U.S., though with a critical caveat: independent tracking by Epoch AI estimates it can only verify 10-20% of total global AI computing capacity, and notes China in particular maintains a large, opaque “dark compute” reserve outside what public tracking can see. The honest answer to “who leads in compute” is that nobody, including researchers who study this full-time, can fully verify the answer.

What This Actually Tells You

“Frontier technology leadership” isn’t a single ranking — it’s at least three separate maps (design, manufacturing, compute) that don’t overlap as cleanly as headlines suggest, plus a meaningful chunk of capacity nobody outside a handful of governments can actually verify. The structural fact that matters most for 2050 isn’t which country currently “leads” by any one of those measures — it’s that the entire global AI buildout currently depends on manufacturing capacity concentrated in one geographically vulnerable location, a single point of failure that no amount of U.S. design dominance or Chinese investment currently offsets.