The Industries Already Pricing In a 2030 Recession

Freight has acted recessionary for three years. Manufacturing just hit a four-year high. The economy can’t agree with itself — and that disagreement is the actual story.

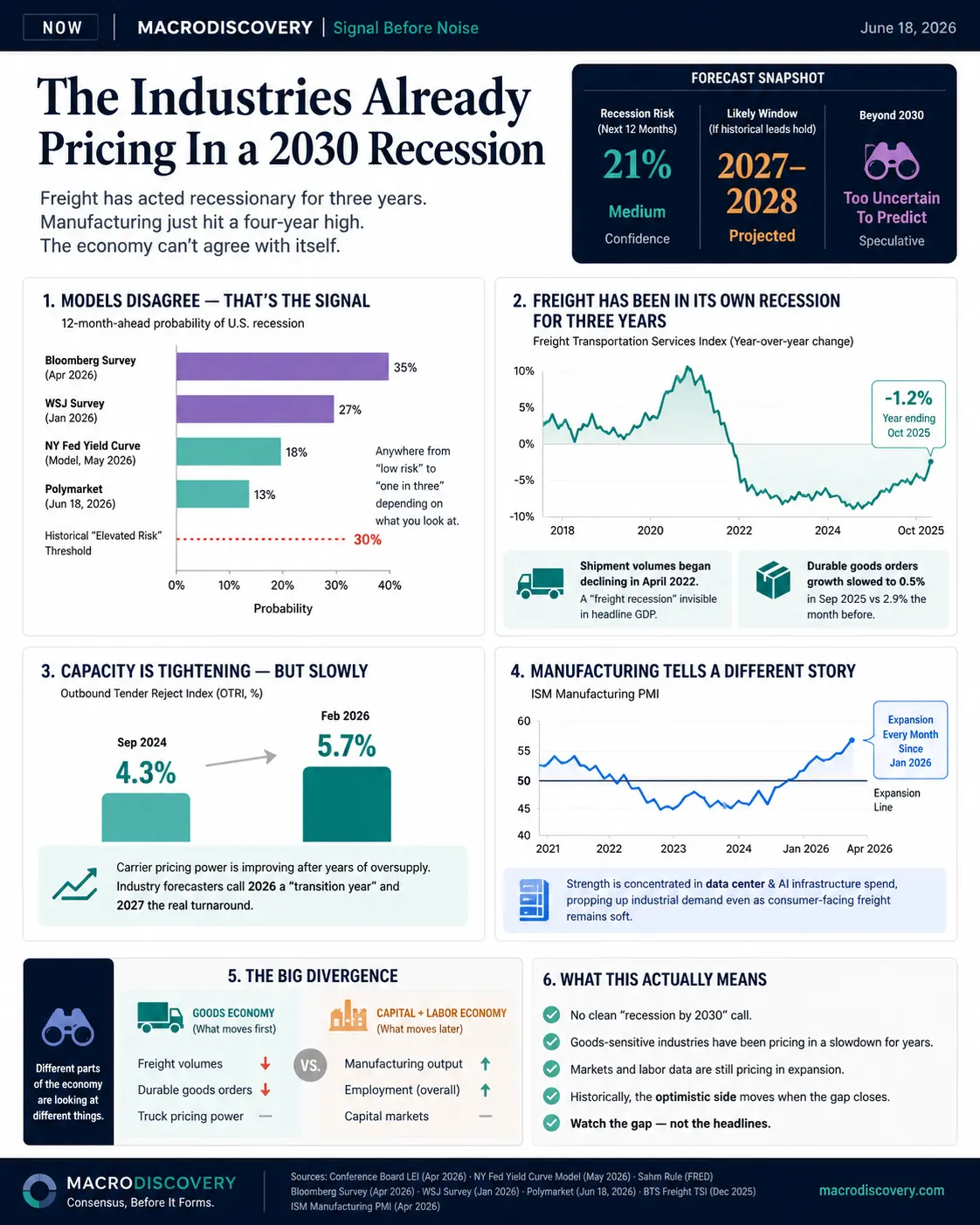

No single number tells this story. The U.S. economy is still growing, unemployment is still low, and most economists still expect 2026 to end without a recession. But a handful of industries — the ones that usually move first — are already behaving like the cycle has turned, well ahead of any official signal.

Known — multiple leading-indicator models are flagging elevated, not extreme, recession risk over the next 12 months, even as headline data still looks expansionary.

Projected — if this cycle’s next downturn follows these models’ own historical lead times, it lands closer to 2027–2028 than 2030.

Speculative — which industries actually lead that downturn, and how deep it runs, isn’t something any current model can tell you.

The Models Disagree With Each Other

The Federal Reserve Bank of New York’s yield-curve model puts the probability of a U.S. recession in the next 12 months at roughly 15–21%, depending on which recent month’s reading you use — elevated relative to a typical expansion, but well short of the 30%+ readings that have preceded every U.S. recession since the late 1960s. The Sahm Rule, a faster-moving labor-market trigger, remains subdued near 0.10, far below the 0.5 threshold that has flagged the start of every recession since 1970 with no false positives. Wall Street’s own surveys split the difference — Bloomberg’s April 2026 consensus put recession odds at 35%, a January 2026 Wall Street Journal poll came in at 27%, and a Polymarket contract on a recession by year-end was trading near 13% as of mid-June.

That spread — anywhere from “low risk” to “one in three” — is itself the story. These aren’t competing predictions so much as different parts of the economy looking at different things.

Freight Has Been in Its Own Recession for Three Years

The clearest example is freight and trucking, which has been signaling distress since long before any headline number moved. Shipment volumes began declining in April 2022, and the sector has spent most of the time since in what analysts openly call a “freight recession” — invisible in broad GDP because services kept growing. The Bureau of Transportation Statistics’ Freight Transportation Services Index fell 1.2% in the year through October 2025, and durable goods orders slowed to 0.5% growth in September 2025, down sharply from 2.9% the month before.

The signal is now turning, but slowly. The Outbound Tender Reject Index — a measure of carrier pricing power — rose from 4.3% in September 2024 to about 5.7% by late February 2026, suggesting capacity is finally tightening after years of oversupply. Meanwhile, the ISM Manufacturing index moved into expansion territory in January 2026 and stayed there every month since — strength that traces in part to one source: data center and AI infrastructure construction propping up industrial demand even while consumer-facing freight stayed soft.

What This Actually Tells You

None of this adds up to a clean “recession by 2030” call, and treating it as one would overstate what these models can do. What it does show is that the industries most exposed to physical goods movement — freight, manufacturing inputs, durable goods — have been pricing in a slowdown for years, while capital markets and labor data are still pricing in an expansion. Historically, when that gap closes, it’s usually the optimistic side that moves, not the pessimistic one. Whether that holds this cycle is the question worth tracking, not predicting.